training, predicting and backtesting Neural Network

-

Hello all, I have several questions. First of all my my code:

I guess my questions arise from the lack of understanding of the backtester, however I will start.

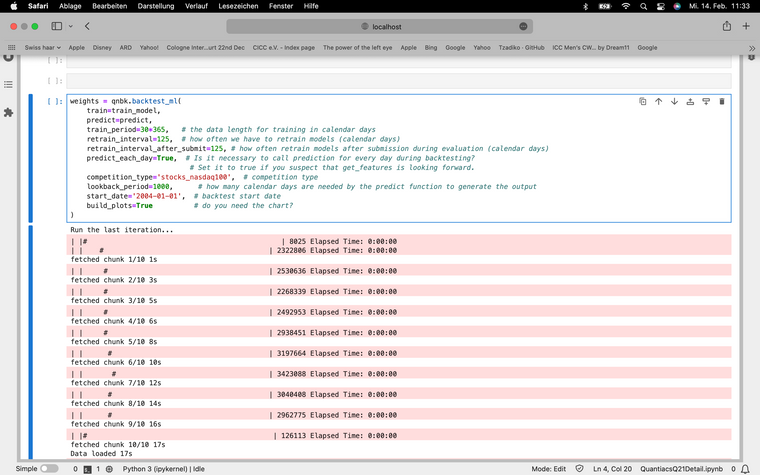

First of all, is it possible to have to not load the data again when predicting, as I am predicting residuals and therefore it seems redundant to load the data twice as its computationally expensive. My next question is regarding the functioning of the backtester in general, my understanding is that: lets assume these are my settings:

the backtester trains the model on the train_period,however it is not clear which dates these are, the latest or furthest away in the past? one the model is trained the prediction part starts, where I do not understand the purpose of lookback as the model is already trained. Thank you very much

-

And a question I forgot. When submitting a strategy, are the weights generated by the backtester the submission weights? As it seems counterintuitive to have have a backtester in a backtester

-

@magenta-kabuto Hi,

-

Yes, it is enough to load the data once at the beginning.

-

The training window in your example is huge, 30 years.....it is a rolling window, and will be used for training your model on a rolling basis. Then the window is shifted forward in time by "retrain_interval", in your case 125 days, and the model is re-trained on the new window.

-

-

@magenta-kabuto The weights generated are simply the daily allocations to the various assets.