Hello !

I'd like to know how to load 2 kind of data such as 'stocks' and 'index' in order to work with Multi-backtesting_ml.

def load_data(period):

stocks = qndata.stocks.load_ndx_data(tail=period)

index = qndata.index.load_data(tail=period)

return stocks, index

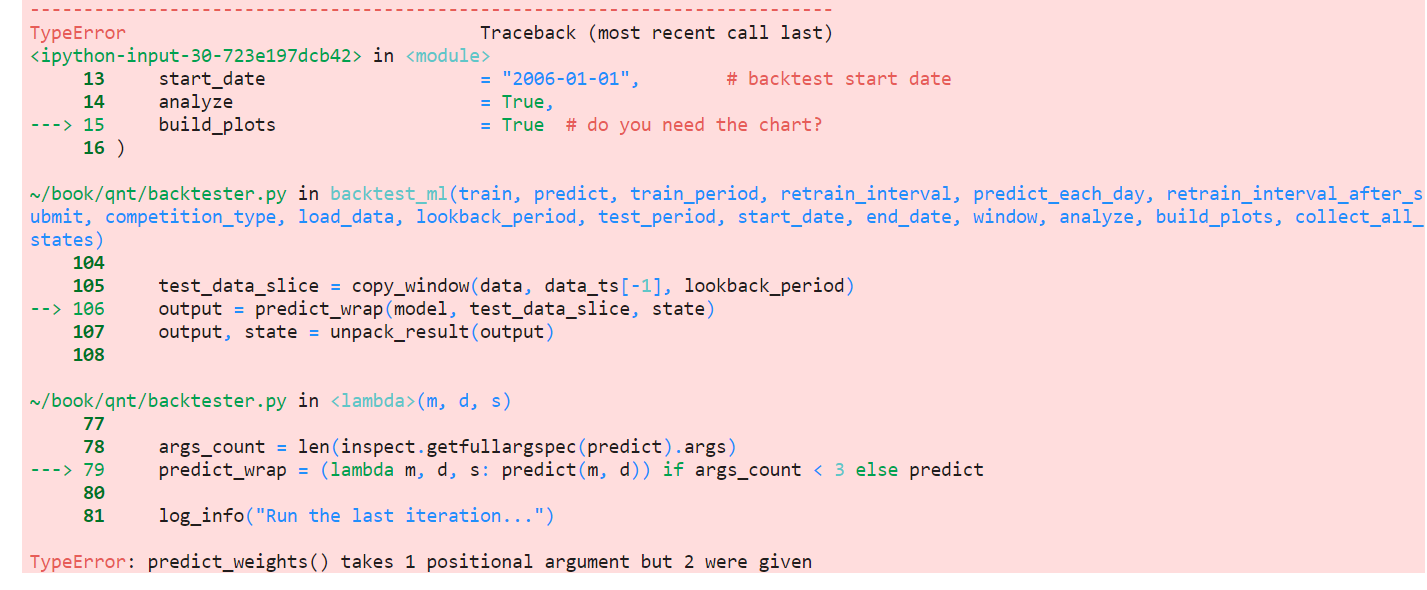

weights = qnbt.backtest_ml(

load_data = load_data,

train = train_model,

predict = predict_weights,

train_period = 15 *365, # the data length for training in calendar days

retrain_interval = 1 *365, # how often we have to retrain models (calendar days)

retrain_interval_after_submit = 1, # how often retrain models after submission during evaluation (calendar days)

predict_each_day = False, # Is it necessary to call prediction for every day during backtesting?

# Set it to True if you suspect that get_features is looking forward.

competition_type = "stocks_nasdaq100", # competition type

lookback_period = 365, # how many calendar days are needed by the predict function to generate the output

start_date = "2006-01-01", # backtest start date

analyze = True,

build_plots = True # do you need the chart?

)

What should I do ?

Best regards,