Has my strategy been rejected from Q23?

-

Hi @support

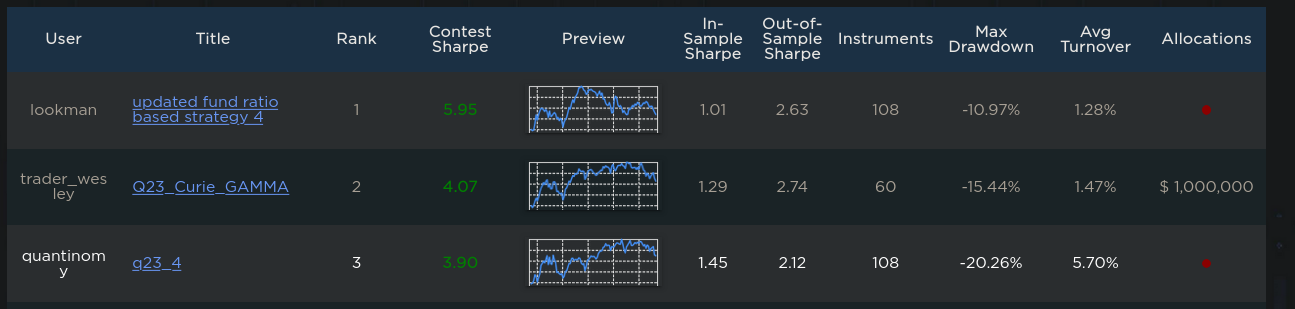

My strategy q23_4 would have made the 3rd place in the Q23 contest but now instead of the allocation there is a red dot whose mouseover reads "The strategy uses manual asset selection or has very high correlation with standard templates; therefore, it has been rejected."

There is definitely no manual selection in any of my strategies and the ones that took part in the contest had to pass the correlation check which also checks against templates.

Could you please tell me what's going on there?

-

Out of curiosity I just cloned the strategy to run it again and see if I get any correlations. And yes:

WARNING! This strategy correlates with other strategies and will be rejected. Modify the strategy to produce the different output. The number of systems with a larger Sharpe ratio and correlation larger than 0.9: 2 The max correlation value (with systems with a larger Sharpe ratio): 0.9818594562862993Then I wanted to know to which strategies it correlates and simply put a

print(json.dumps(cr_list, indent=4))insideqnt.stats.check_correlationand got this:[ { "id": 18701501, "name": null, "my": false, "template": false, "cofactor": 0.9818594562862993, "sharpe_ratio": 2.364183164325061 }, { "id": 18701502, "name": null, "my": false, "template": false, "cofactor": 0.9559821139736059, "sharpe_ratio": 2.49988419656187 } ]The first one is my q23_4 and the other one is my q23_4a (funny that it correlates with itself by 0.98 and not 1.0). However, no correlation with any template is showing up there.

-

@antinomy Dear antinomy, thanks for the comment. We believe that there is a problem with the asset selection in your submission. The Q23 contest is aimed to trade assets belonging to the full SP500 universe, it is not a Nasdaq-100 contest.

-

@support

Thanks for your reply.My strategy trades a subset of assets from the S&P 500 universe, selected with certain filter rules. Most are technical and one of them is that they also belong to the Nasdaq 100 index.

Which contest rule would be violated when a strategy selects stocks which are part of the contest universe and also part of another index?Is selecting assets based on them being part of an index considered as "manual selection"? This would mean every strategy for all the Nasdaq 100 and S&P 500 contests is against the rules and the contest rules would contradict themselves.

-

And what if a strategy uses the following rules to select assets to trade:

- the primary exchange is NAS

- the sector is not finance

- has price data for at least the previous 3 months

- has an average daily trading volume of at least 200 k based on the previous 3 months

- belongs to the top 100 of the thus far selected assets in terms of market capitalization

Would you say any of these rules violate the contest rules?

Because these are the selection criteria for the N100 constituents. The only difference in my strategy is that I'm using

qnt.data.stocks_load_ndx_data.sel(field='is_liquid')instead.

Sure, the first of the rules above manually selects the exchange and the second one manually excludes a sector. But still none of these manually select assets and neither does the filteris_liquidfrom another dataset.Also, lets take a look why you prohibited manual asset selection in the first place. Wasn't this to avoid lookahead bias? And isn't this also the reason for the existence of the field

is_liquidin any of your datasets? Are you saying that the exact field you introduced to avoid lookahead bias is now the reason you disqualify a strategy because of lookahead bias just because it's from a dataset other than the one for the contest?