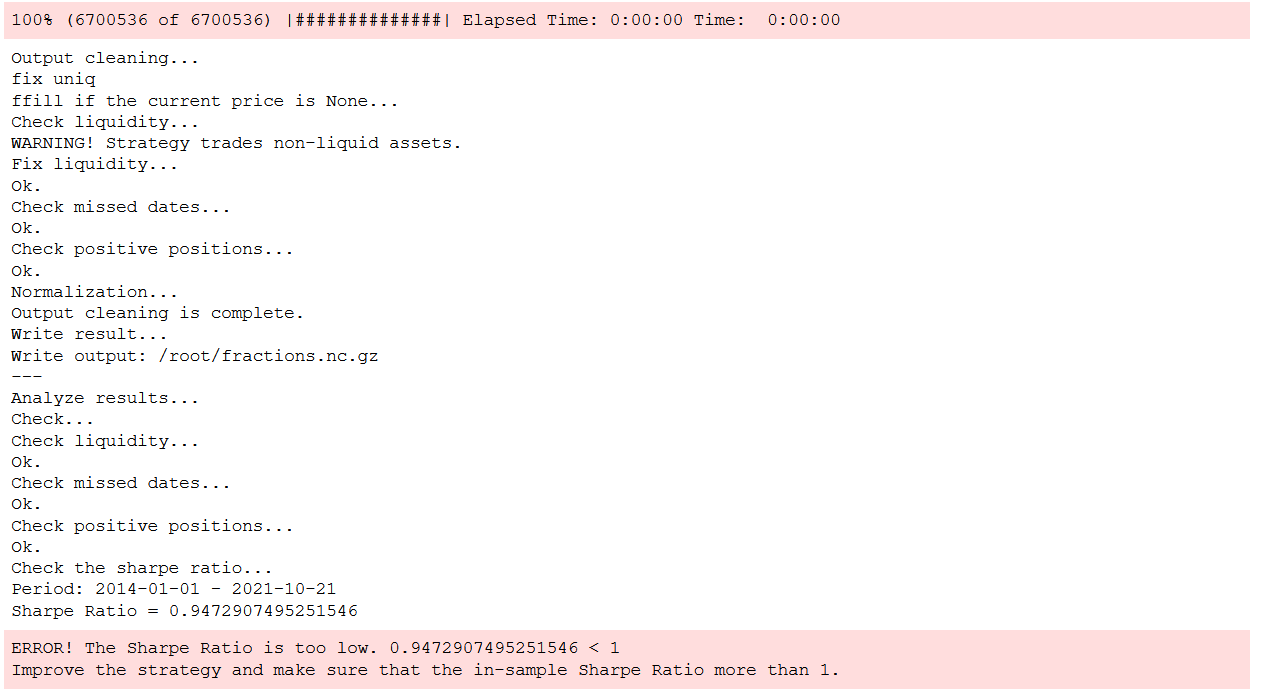

Hi

Just want to clarify 2 things:

-

For crypto futures competition, we still need to get data from: qndata.cryptofutures.load_data(tail=period)

or this: qndata.crypto.load_data(tail=period, assets="BTC") -

The data from qndata.cryptofutures.load_data() is daily level whereas the data in qndata.crypto.load_data() is hourly, so are the strategies judged with daily level data?

file:///home/anshul/Pictures/Screenshot%20from%202022-04-29%2002-39-18.png

file:///home/anshul/Pictures/Screenshot%20from%202022-04-29%2002-39-18.png