@support i see. Can you update the website in above screen to avoid confusion please

A

Posts made by angusslq

-

RE: Q23 should be running now, but not able to join, right?posted in Support

-

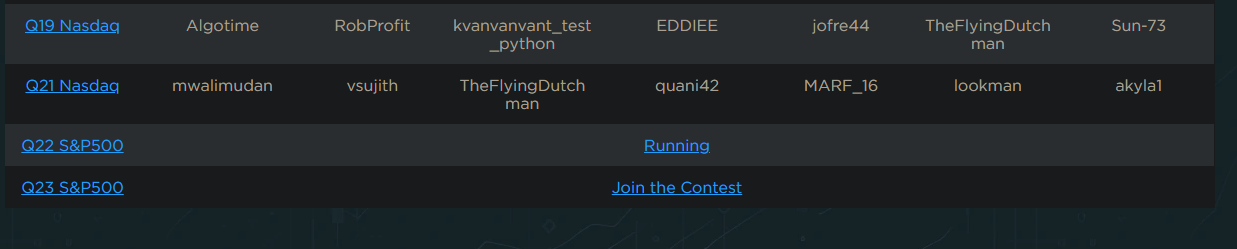

Q23 should be running now, but not able to join, right?posted in Support

I though i still be able to join from the page there, but it is actually not able to join.

@support , can you help to update the website for that?

-

RE: Q22 seems paused at 22-may, is it expected?posted in Support

@support great! i can see the latest result. Do you know when Quantiacs will announce the Q22 result formally? Thanks.

-

Q22 seems paused at 22-may, is it expected?posted in Support

Hi @support ,

it seems to me that Q22 paused at 22-may and no longer updated since 2 weeks, is Q22 still undergoing some technical issue? is it expected?

Thanks. -

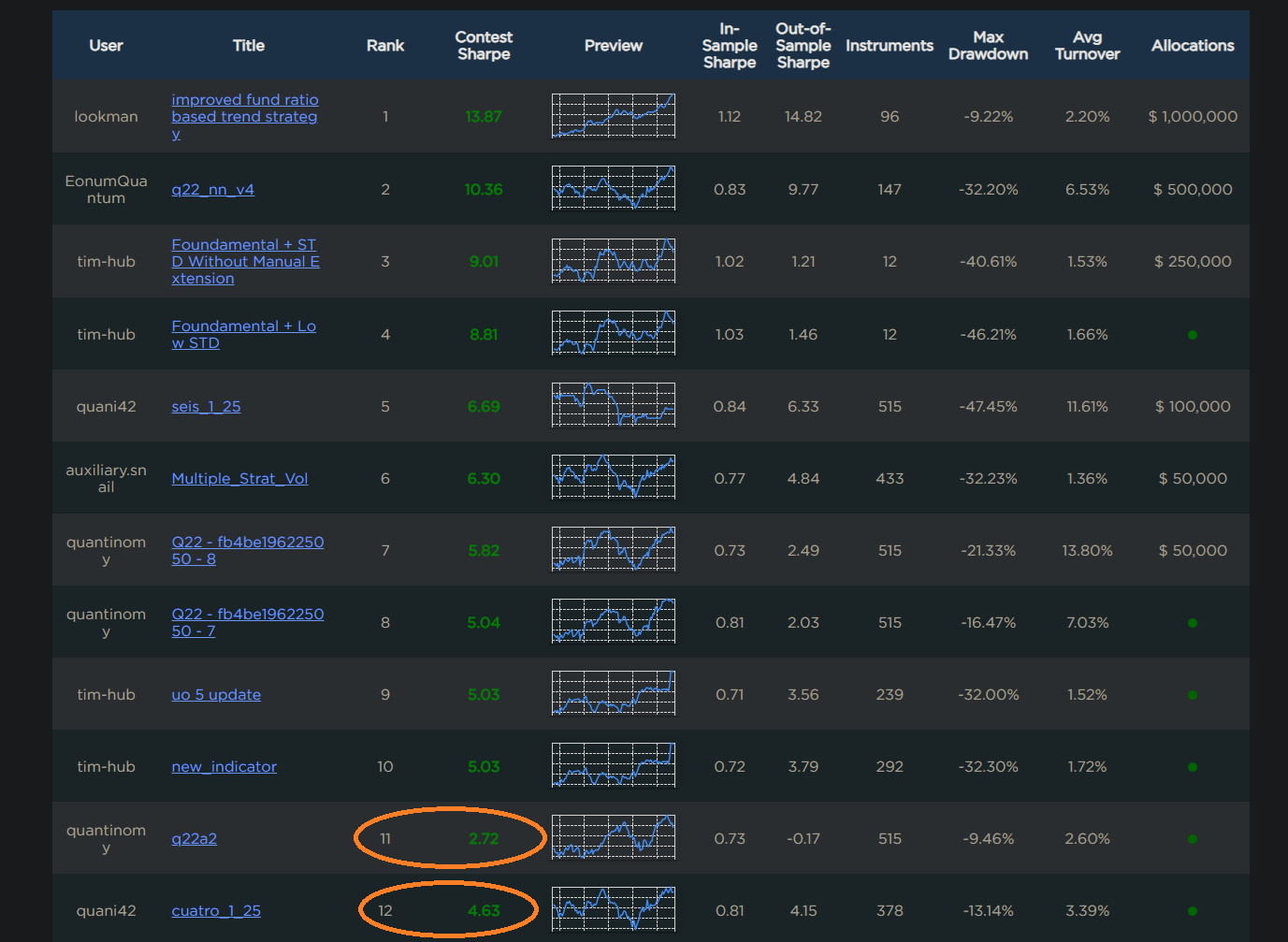

Why a lower contest sharpe can rank higher than higher contest sharpe?posted in Support

for example, 2.72 contest sharpe ranked 11 but 4.64 contest sharpe ranked 12

Besides contest sharpe, what's the factor for ranking please?

-

RE: Question about the contest structureposted in Support

@support may i know why the sharpe ratio doesn't take into account for risk free return (e.g. https://www.investopedia.com/terms/s/sharperatio.asp)?

It is weird that a strategy that return is less than risk free return can win

-

RE: Question about the contest structureposted in Support

@support said in Question about the contest structure:

at the end of that period the prizes will be given to the winners.

what's the prize referring to? is it 10% profit of the allocated amount of money to the algo? if that is the case, does that mean the amount allocated will change every day according to the ranking?

e.g.17-Feb user A is 1st => allocated 1M

17-Feb user B is 2nd => allocated 0.5Mprize for 17-Feb is 10% of daily profit according to above allocation.

18-Feb user C is 1st => allocated 1M

18-Feb user A is 2nd => allocated 0.5Mprize for 18-Feb is 10% of daily profit according to above allocation?

-

Q18 Quick start guide not working anymoreposted in Support

I am currently trying to retry multi data set. i follow the example of Q18 and change for spx / s&p500. However, it doesn't work anymore. May i know how can i return multi data set in Q22 now? Thanks a lot.

https://quantiacs.com/documentation/en/examples/q18_quick_start.html

def load_data(period): futures = qndata.futures.load_data(tail=period, assets=["F_DX"]).isel(asset=0) stocks = qndata.stocks.load_spx_data(tail=period) return {"futures": futures, "stocks": stocks}, futures.time.values qnbt.backtest( competition_type= "stocks_s&p500", load_data= load_data, lookback_period= 365, start_date= "2006-01-01", strategy= strategy, window= window )Error happened in validate_data function

File ~/book/qnt/backtester.py:386, in backtest.<locals>.validate_data(data) 377 def validate_data(data): 378 mismatches = { 379 'stocks': ['stocks', 'stocks_long'], 380 'stocks_s&p500': ['stocks_s&p500'], (...) 384 'futures': ['futures'] 385 } --> 386 if data.name not in mismatches.get(competition_type, []): 387 log_err( 388 f"WARNING! The data type and the competition type are mismatched. Data type: {data.name}, competition type: {competition_type}") AttributeError: 'tuple' object has no attribute 'name' -

Is the server busy? my job didn't start after 2 days still, is it normal?posted in Support

Is the server busy? my job didn't start after 2 days still, is it normal?

-

Calculation time exceeded questionposted in Support

May i know what’s the calculation time definition?

The contest t&c is not quite clear to me.

The execution time of your code must be less than 10 minutes per each point in time.“Per each point of time”

Is it referring to the duration of time for a given date?

Thanks for advice

-

RE: datatype for weights seems changed recentlyposted in Support

@stefanm Thank you for the details

-

datatype for weights seems changed recentlyposted in Support

weights = qnbt.backtest( competition_type="stocks_s&p500", load_data=load_data, lookback_period=350, start_date="2006-01-01", strategy=strategy, window=window, analyze=True, check_correlation=False )In the old days, i can write using as below as per documentation

qnout.write(weights)Since some days ago, the above doesn't work, i need to change to

qnout.write(weights[0])to make it work again, does it expect? @support

-

RE: Strategy filtered after a few daysposted in Strategy help

Below is the log. there is conda related error (but the calculation completed still). Is it causing the strategy filtered? Is there any solution for this please

Error while loading conda entry point: conda-libmamba-solver (libarchive.so.20: cannot open shared object file: No such file or directory) /usr/local/lib/python3.10/site-packages/conda/base/context.py:982: FutureWarning: Adding 'defaults' to the channel list implicitly is deprecated and will be removed in 25.3. To remove this warning, please choose a default channel explicitly via 'conda config --add channels <name>', e.g. 'conda config --add channels defaults'. deprecated.topic( Error while loading conda entry point: conda-libmamba-solver (libarchive.so.20: cannot open shared object file: No such file or directory) http://hl.datarelay:7070/last/2024-12-23T00/ https://stat.quantiacs.io/regular/task/316264333663616565643330663366393465636265393364353364313431653635343437396363643661393335303666383033653663626336303761316634623A313733353339313431343A3230323431373431/ Calculation start... [NbConvertApp] Converting notebook strategy.ipynb to html [NbConvertApp] Writing 294586 bytes to strategy.html Calculation completed. -

Strategy filtered after a few daysposted in Strategy help

Hi,

I had a strategy submitted for around 5days and it was submitted successfully (at least i can see my entry in leaderboard). But after the weekend i found my strategy in filtered tab and no longer can be found in leaderboard. My strategy id is # 17958989I checked that there is no error reported in the log can @support or anyone please help to have a look and point me the way to resolve it please

Thank you