Hi all,

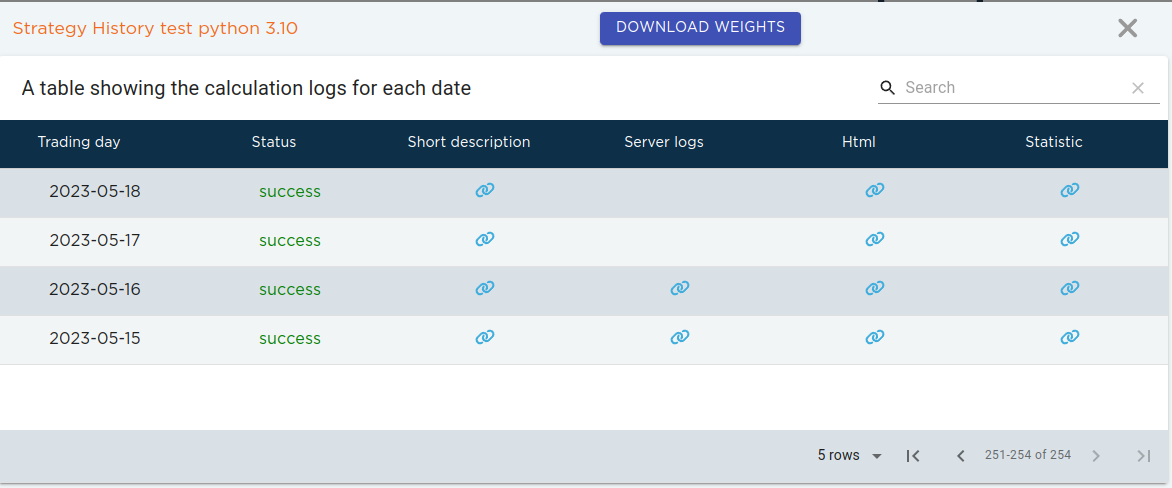

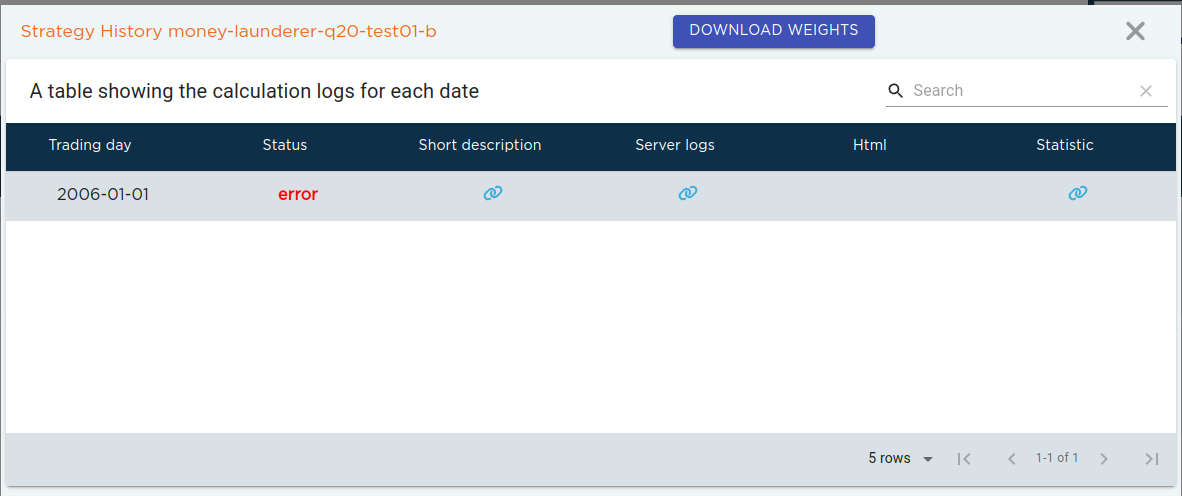

I'm fairly new just trying to learn. I wanted to submit some test strategy which was all good locally and in the online environment with sr>1 with multipass test. However when I submitted it seemed it was not even executed? Here are the logs (which is obscure tbh)

INFO: 2023-09-11T23:35:42Z: pass started: 15136753

INFO: 2023-09-11T23:35:44Z: nxt: 2006-01-03T00:00:00Z

INFO: 2023-09-11T23:35:44Z: next date: 2006-01-03T00:00:00Z

INFO: 2023-09-11T23:35:47Z: nxt: 2006-01-03T00:00:00Z

INFO: 2023-09-11T23:35:47Z: next date: 2006-01-03T00:00:00Z

INFO: 2023-09-12T00:15:45Z: stats received light=false

INFO: 2023-09-12T00:15:45Z: progress: 0.0

INFO: 2023-09-12T00:15:45Z: checking: first pass

INFO: 2023-09-12T00:15:45Z: filter passed: source exists

INFO: 2023-09-12T00:15:45Z: filter passed: output html exists

FAIL: 2023-09-12T00:15:45Z: filter failed: output missed

INFO: 2023-09-12T00:37:46Z: pass completed: 15136753

server log

statistics:

{"id":14162495,"series":[],"submission_id":"15136749","output_exists":false,"source_exists":true,"last_data":true,"non_liquid":null,"trades_only_btc":null,"output_dates_missed":false,"exposure_check_succeed":null,"ref_output":null,"html_gz":null,"correlated_list":[],"ref_date":1136073600000,"last_date":null,"light":false,"state":null}

Can you please help me know what was the issue?