@vyacheslav_b Thank you for responding.

I realize that even now I have a strategy that is not forward-looking

close = data.sel(field="close")

price_yesterday = qnta.shift(close, 1)

target_price_up = xr.where((price_yesterday < close), 1, 0)

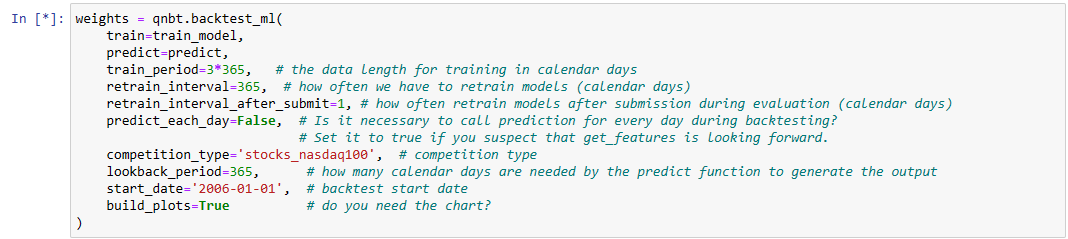

Why is Sharpe worse after the strategy goes through training-testing by ML/DL models compared to when using a single backtest?

I have tried many different strategies and changed different feature trains, but they all showed that after going through a certain model, the sharpness decreased compared to when using a single backtest. Please answer. Thank you so much.