Hello,

I have a question regarding my strategy. I defined a trading strategy and in [10] for each Asset listed in the Nasdaq, applied that strategy for the close values for a given time period.

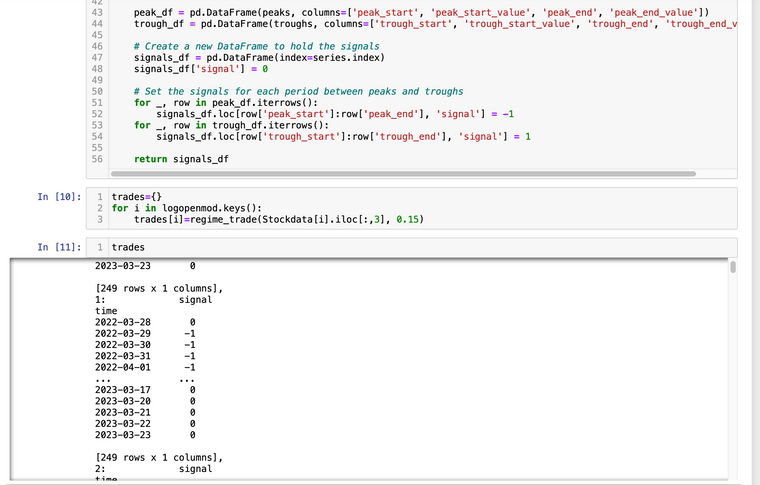

The signals of each asset are saved in a pandas dataframe with datetime index, which are the saved in a dictionary.

Now it is not clear to me, from the examples given on the page, how to pass this into the qnt backtest.

I will be thankful, if anyone can help me out on this. Thx

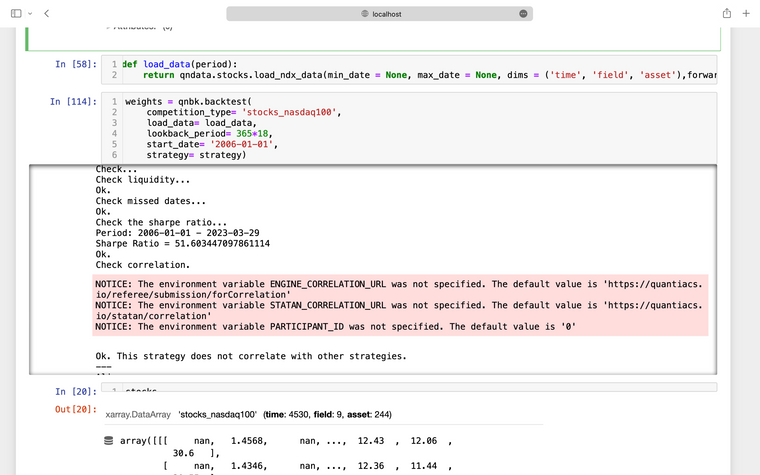

As you can see in the picture I have a good sharpe Ratio but when submitted ,the strategy got rejected because the sharpe ratio is too low. If I assume there is no bug in your multipass backtest, the issue should be the statelessness of your backtester. I tried to correct the code and to my understanding it should be fine but I dont know, and if I only rely on getting the news after submission, I will miss the deadline. Could you therefore pls have a look at the notebook too and if it does not take too much time correct anything if possible. Thank you. Regards

As you can see in the picture I have a good sharpe Ratio but when submitted ,the strategy got rejected because the sharpe ratio is too low. If I assume there is no bug in your multipass backtest, the issue should be the statelessness of your backtester. I tried to correct the code and to my understanding it should be fine but I dont know, and if I only rely on getting the news after submission, I will miss the deadline. Could you therefore pls have a look at the notebook too and if it does not take too much time correct anything if possible. Thank you. Regards

")