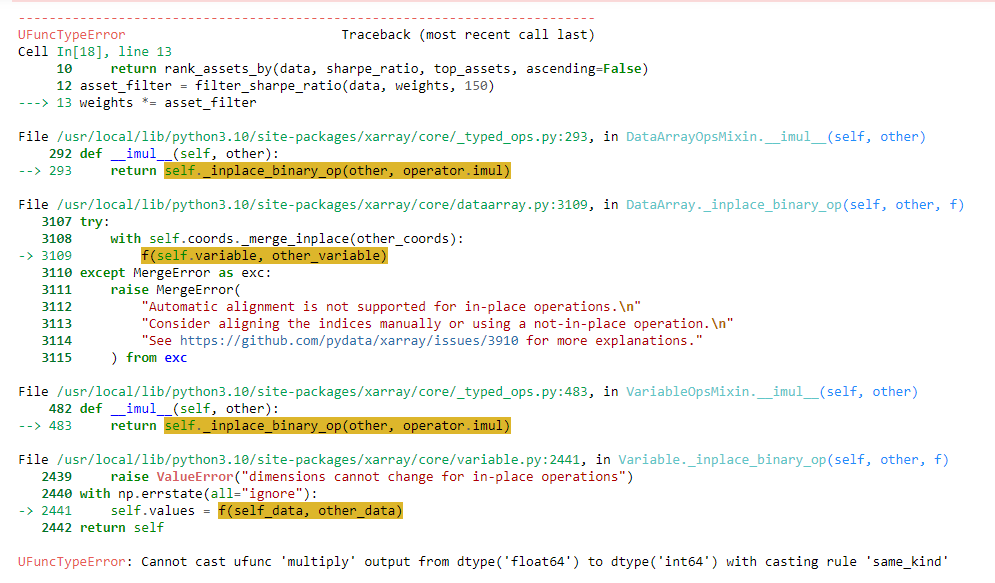

Cannot cast ufunc 'multiply' output from dtype('float64') to dtype('int64') with casting rule 'same_kind'

-

Hi, I'm testing the new ticker filtering methods that Quantiacs provides, but I'm getting the error Cannot cast ufunc 'multiply' output from dtype('float64') to dtype('int64') with casting rule 'same_kind'

This is my code

# Import basic libraries. import xarray as xr import pandas as pd import numpy as np # Import Quantiacs libraries. import qnt.data as qndata # load and manipulate data import qnt.output as qnout # manage output import qnt.backtester as qnbt # backtester import qnt.stats as qnstats # statistical functions for analysis import qnt.graph as qngraph # graphical tools import qnt.ta as qnta # indicators library import qnt.xr_talib as xr_talib # indicators library data = qndata.stocks.load_ndx_data(min_date="2005-06-01") def filter_volatility(data, rolling_window, top_assets, metric="std", ascending=True): """ Filter and rank assets based on volatility over a rolling window. Args: data (xarray.Dataset): The dataset containing asset data. rolling_window (int): Window size for the rolling volatility computation. top_assets (int): Number of top assets to select. metric (str): Volatility metric to use ('std' for standard deviation). ascending (bool): Rank order, True for lowest first. """ prices = data.sel(field='close') daily_returns = prices.diff('time') / prices.shift(time=1) rolling_volatility = calc_rolling_metric(daily_returns, rolling_window, metric) volatility_ranks = rank_assets_by(data, rolling_volatility, top_assets, ascending) return volatility_ranks def calc_rolling_metric(condition, rolling_window, metric="std"): """ Compute a rolling metric (standard deviation or mean) over a specified window for a given condition. Args: condition (xarray.DataArray): Data over which the metric is computed. rolling_window (int): Window size for the rolling computation. metric (str): Type of metric to compute ('std' for standard deviation, 'mean' for average). Raises: ValueError: If an unsupported metric is specified. """ if metric == "std": return condition.rolling({"time": rolling_window}).std() elif metric == "mean": return condition.rolling({"time": rolling_window}).mean() else: raise ValueError(f"Unsupported metric: {metric}") def rank_assets_by(data, criterion, top_assets, ascending): """ Rank assets based on a specified criterion. Returns a DataArray where top ranked assets are marked with a '1'. Args: data (xarray.Dataset): The dataset containing asset data. criterion (xarray.DataArray): The data based on which assets are ranked. top_assets (int): Number of top assets to select. ascending (bool): True for ascending order, False for descending order. """ volatility_ranks = xr.DataArray( np.zeros_like(data.sel(field='close').values), dims=['time', 'asset'], coords={'time': data.coords['time'], 'asset': data.coords['asset']} ) for time in criterion.coords['time'].values: daily_vol = criterion.sel(time=time) ranks = (daily_vol if ascending else -daily_vol).rank('asset') top_assets_indices = ranks.where(ranks <= top_assets, drop=True).asset.values volatility_ranks.loc[dict(time=time, asset=top_assets_indices)] = 1 return volatility_ranks.fillna(0) close = data.sel(field="close") sma_slow = qnta.sma(close, 200) sma_fast = qnta.sma(close, 20) weights = xr.where(sma_slow < sma_fast, 1, -1) def filter_sharpe_ratio(data, weights, top_assets): stats_per_asset = qnstats.calc_stat(data, weights, per_asset=True) sharpe_ratio = stats_per_asset.sel(field="sharpe_ratio") return rank_assets_by(data, sharpe_ratio, top_assets, ascending=False) asset_filter = filter_sharpe_ratio(data, weights, 150) weights *= asset_filter # Liquidity filter and clean is_liquid = data.sel(field="is_liquid") weights = weights * is_liquid weights = qnout.clean(weights, data, "stocks_nasdaq100") stats = qnstats.calc_stat(data, weights.sel(time=slice("2006-01-01", None))) display(stats.to_pandas().tail()) performance = stats.to_pandas()["equity"] qngraph.make_plot_filled(performance.index, performance, name="PnL (Equity)", type="log") weights = weights.sel(time=slice(date,None)) qnout.check(weights, data, "stocks_nasdaq100") qnout.write(weights) # to participate in the competition

Besides I couldn't import the qnfilter library so I had to call the function directly from the strategy. Looking forward to your support. Thank you

-

@machesterdragon said in Cannot cast ufunc 'multiply' output from dtype('float64') to dtype('int64') with casting rule 'same_kind':

weights *= asset_filter

Hello. Change

weights *= asset_filterto

weights = weights * asset_filterYou can see usage examples here:

https://quantiacs.com/documentation/en/user_guide/dynamic_assets_selection.htmlEverything is working correctly now, try cloning the strategy.