Competition filters¶

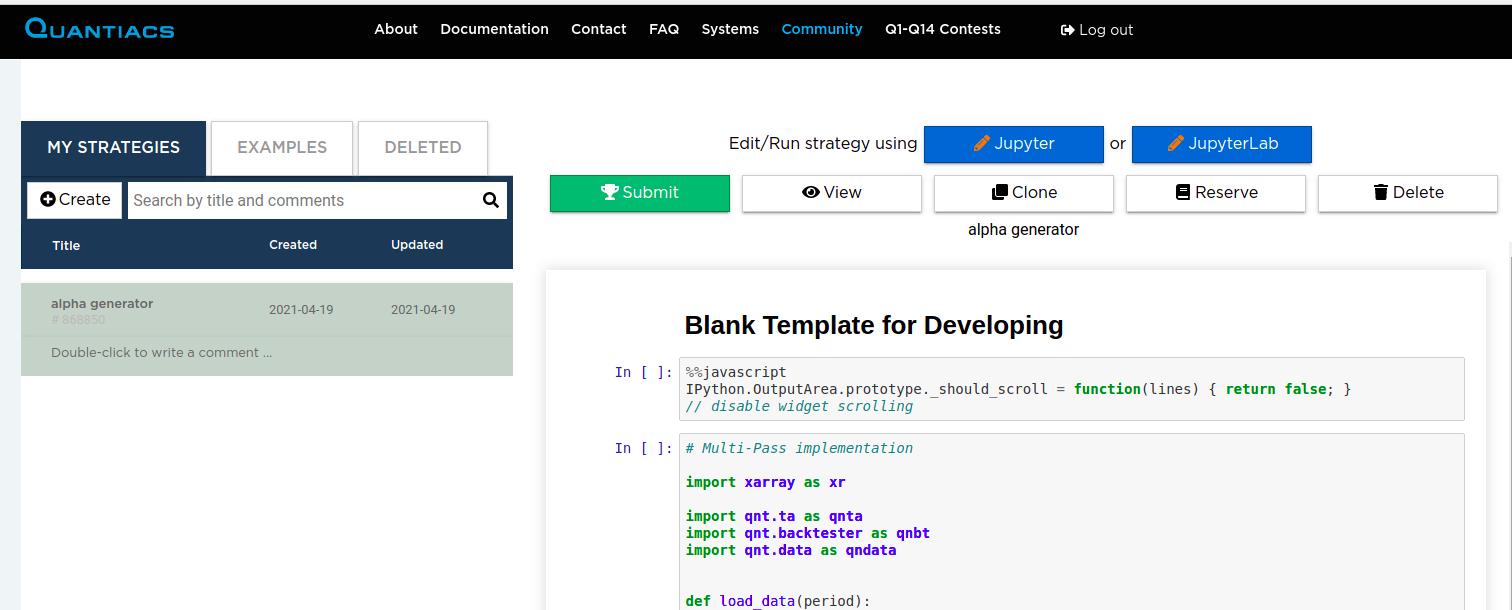

To submit a strategy to the contest, click the Submit button in your Development area:

You can also submit code directly from your development environment in Jupyter Notebook or JupyterLab.

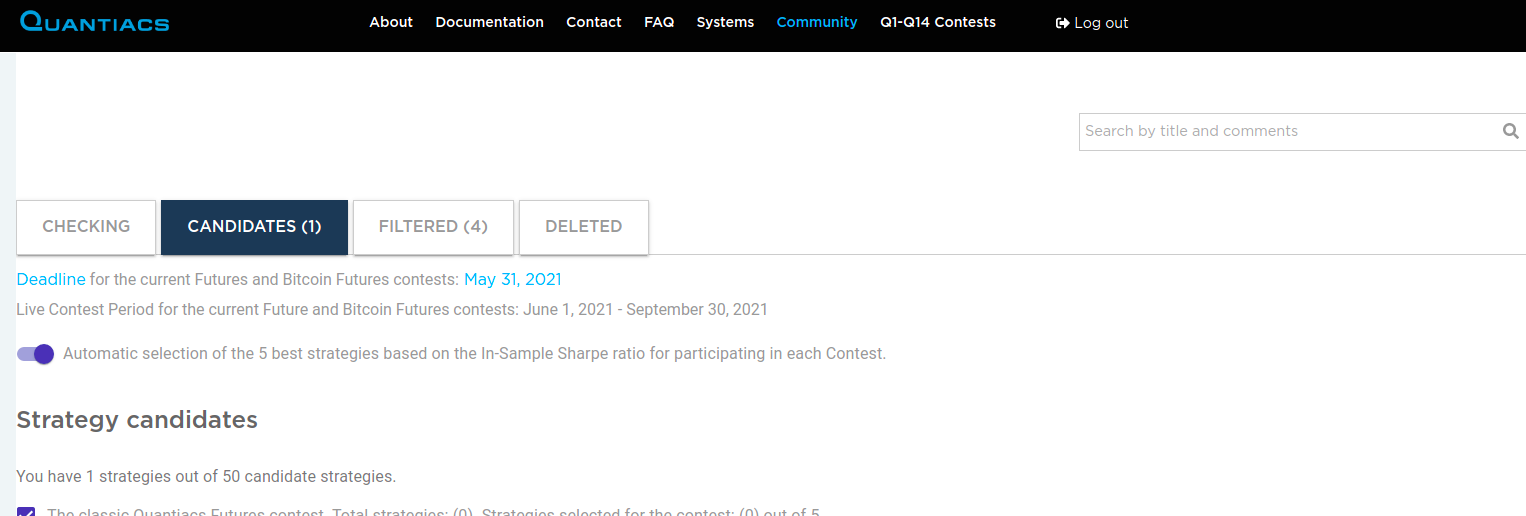

After submission, our servers check your code. The status appears in the Competition section of your account, under the Checking tab:

If your algorithm passes these checks (filters), it is admitted to the Contest and appears under the Candidates tab. If it fails, it is listed under the Filtered tab, where you can inspect the logs to see what went wrong.

Technical filters¶

Source file must exist¶

An error saying strategy.ipynb was not found means your strategy file has a non-standard name. It must be named strategy.ipynb.

Execution failed¶

If strategy.ipynb fails to execute, check the logs (server logs and html columns) for details on what went wrong.

Pay special attention to the dates in the logs: you can use this information to reproduce the problem in the precheck.ipynb file you find in your root directory. Substitute these dates when calling evaluate_passes.

Weights must be written¶

If you see Missed call to write_output, your strategy is not saving the final weights. The last call in strategy.ipynb should be qnt.output.write(weights) (or qnt.backtest(…) if you use multi-pass backtesting), assuming weights holds your final allocation.

qnt.output.write(weights)

All data must be loaded¶

An error saying data is loaded only until a certain day means you are cropping the date range. Do not crop data when you submit, because your system needs to run daily on new data.

Error:

qndata.futures.load_data(min_date="2006-01-01", max_date="2008-01-01")

Solution

qndata.futures.load_data(min_date="2006-01-01")

Weights must be generated for all trading days¶

An error saying the strategy does not have weights for all trading days means weights for some days are missing, for example because of a drop operation. Avoid this by using qnt.output.check(weights, data, “futures”) (assuming you are working with futures and generating weights on data).

Weights are not generated at the beginning of the time series¶

Your strategy must produce non-zero weights from the start date defined for each contest:

NASDAQ-100 Contest - Trading should begin from January 1, 2006.

Futures Contest - Trading should begin from January 1, 2006.

Bitcoin Futures - Trading should start from January 1, 2014.

Crypto Top-10 Long - Trading should commence from January 1, 2014.

Review your strategy code:

Verify the data range being loaded. Define the appropriate time frame as follows:

futures = qndata.futures.load_data(min_date="2006-01-01")

Ensure the data range being saved:

display(weights) qnt.output.write(weights)

The Sharpe ratio computation starts from the date of the first non-zero weights. If your algorithm starts generating weights on Bitcoin Futures from January 1, 2017, it will not be accepted because the In-Sample period is too short.

This often happens when technical analysis indicators need a warm-up period. You can check the date with:

min_time = weights.time[abs(weights).fillna(0).sum('asset')> 0].min()

min_time

The value of min_time should be equal to or later than the starting date specified in the rules for the respective competition.

If min_time is later than the starting date, it’s recommended to fill the starting values of the time series with non-zero values. For instance, you could use a simple buy-and-hold strategy.

def get_enough_bid_for(data_, weights_):

time_traded = weights_.time[abs(weights_).fillna(0).sum('asset') > 0]

is_strategy_traded = len(time_traded)

if is_strategy_traded:

return xr.where(weights_.time < time_traded.min(), data_.sel(field="is_liquid"), weights_)

return weights_

weights_new = get_enough_bid_for(data, weights)

weights_new = weights_new.sel(time=slice("2006-01-01",None))

For details on the calculation method, see the source code in qnt.output.calc_sharpe_ratio_for_check.

Timeout¶

An error saying the strategy calculation exceeds the time limit means you need to optimize your code. Futures systems must finish within 10 minutes, and Bitcoin futures/Crypto long systems within 5 minutes.

Number of strategies¶

An error about the strategy limit means you have too many running strategies. You can have at most 50, and you should select 15 for the contest.

Templates¶

A copy of a template will NOT be eligible for a prize.